Do you wonder if you’re at risk of owing estate tax? If so, which assets will you pay the tax on? It comes down to what is considered “in” your estate and what is considered “out” of your estate. You pay tax on assets in your estate, and you don’t pay tax on assets out of your estate.

So, what’s in versus out of your estate?

Let’s look briefly at the estate tax, what’s considered in and out of your estate, and a few ideas on how you can move an asset out of your estate. We’ve also included the video below to help walk through this topic.

How does the estate tax work?

The estate tax is a tax assessed by the federal government and some state governments on your accumulated wealth when you die.

- The federal tax starts at 18% on your first taxable $10,000, increasing to 40% on taxable assets over $1 million.

- You and your spouse can each pass $15 million tax-free – called an “exemption” – for a total of $30 million before owing any federal estate tax, the highest exemption in history.

Many states, including Washington, add an additional estate tax. In WA State, your first $3 million passes tax free. Then, the tax rate starts at 10% for the first taxable $1 million and climbs to 35% for taxable assets above $9 million.

What’s in vs. out of your estate?

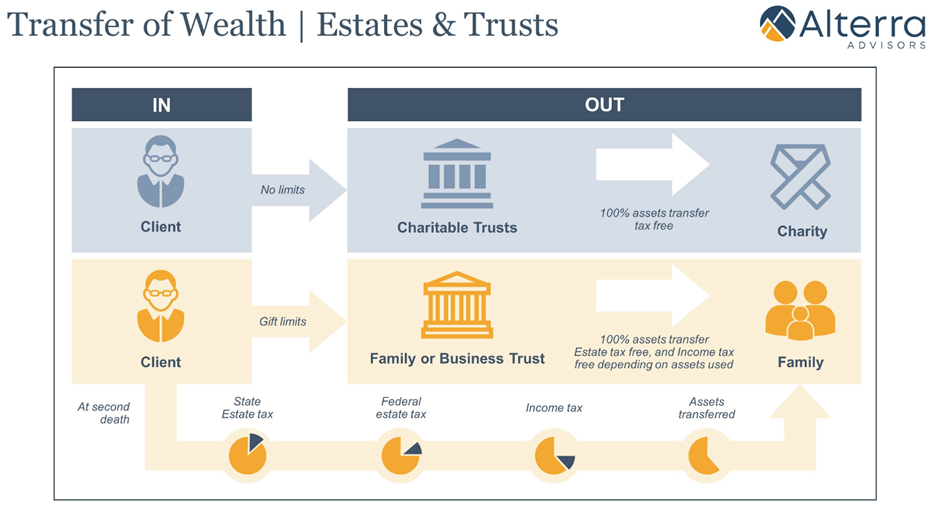

To better understand what gets taxed, let’s cover some basic concepts using the diagram below.

- Assets IN your estate. Your estate is the total of everything you personally own – the left column. These assets “in your estate” are subject to taxes as described above.

- Assets OUT of your estate. While your assets start “in your estate”, you can move many assets out of your estate – the right column – avoiding estate tax by giving them to certain kinds of trusts.

A few things to note about how your estate passes:

- The government takes their cut first. In orange, we see that state estate tax, federal estate tax, and income taxes are paid from your estate before the remainder goes to your family. A wide range of trusts and transfer strategies can reduce taxes and pass more to loved ones.

- Nothing passes to charity by default, you must act to give to charity. In blue, we see that there are no limits to what you can pass tax-free to charity, but this doesn’t happen automatically. Strategies like Charitable Remainder Trusts can even pay income to you today, reduce estate taxes, and leave a gift to charity.

- Moving assets out of your estate doesn’t always mean giving up full access. As we discuss in Out of Your Estate, Not Out of Reach, you can reduce taxes without losing full control of your assets.

Where should you start?

We all start with a plan by default…the government’s plan. With knowledge about what’s “in” your estate and what’s “out” of your estate, you start making a proactive plan – a plan by design.

For more ways to reduce your estate, see our videos on 5 Ways to Reduce Estate Taxes and Pass More to Your Family and 4 Ways to Reduce Estate Taxes and Pass More to Charity!

While most plans require a team of financial, legal, and tax professionals, a conversation with a comprehensive financial planning team, like ours at Alterra, is a great place to start. Before you have wills and trusts drafted, you’ll want a clear, coordinated action plan for the big picture. With a plan in hand, you’ll be well on your way to reducing loss to estate taxes and passing more to the people and causes you care about! Learn more about How We Work.

Alterra Advisors does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.

Zach Hamilton

CFP®

Partner, Financial Advisor

About the Author

Zach graduated from Gonzaga University with degrees in Marketing and Finance. While growing up, Zach heard stories from his grandfather about his work as an insurance agent, and other stories from his dad who was an investment manager. They both spoke financial “languages” but had completely different dialects. Recognizing the breadth of the financial vocabulary ultimately led to Zach’s passion for financial planning. He credits his family for this enthusiasm. Zach sees his time with clients as an opportunity to translate all of the different – and often confusing – information they’ve heard and provide clear guidance for each unique situation.

Zach enjoys working with people – his clients – who also appreciate that their financial decisions have an impact not just on themselves, but also on their families, charities and their own life legacy. Many of Zach’s clients have a strong desire to “make a difference”, and they rely on his financial expertise to magnify their philanthropic goals.

The “Alterra” name was coined by joining the Latin roots “alter”, the origin of the word “altruism” with “terra” meaning earth or land. This name reflects the company philosophy of “clients before profits” and providing firmly grounded advice.