We’ve all felt it—that sinking feeling when markets dip and headlines scream uncertainty. Suddenly, all those mantras—“time in the market beats timing the market,” “stay the course,” “ride it out”—start to feel more like blind optimism than sound strategy.

But those mantras exist for a reason. History shows us that, even through recessions, bubbles, pandemics, and political chaos, markets have consistently recovered—and rewarded those who stayed disciplined.

Why Volatility Feels Worse Than It Is

Take a step back. Over decades, the stock market has climbed steadily. But zoom in on any crisis—the dot-com bust in 2000, the 2008 financial crisis, or even the COVID crash—and you’ll see just how emotionally turbulent the ride can be.

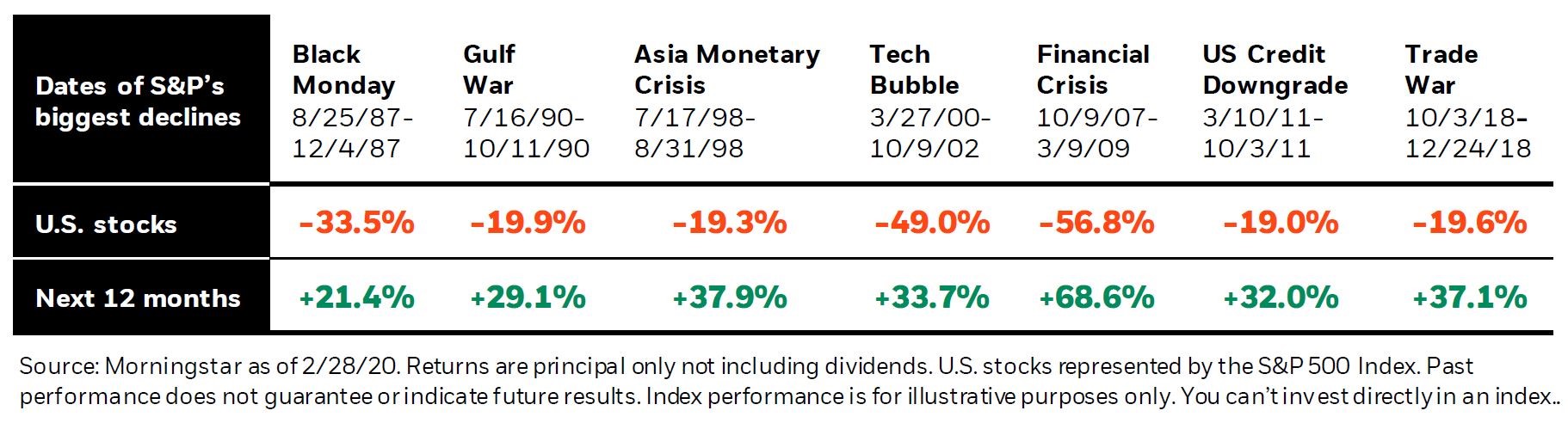

In those sharp declines, the instinct is almost universal: “Maybe I should get out now and get back in when things feel more stable.” But “stability”, usually indicated by a significant market rebound, returns with surprising speed—and without warning. Below, you’ll see seven of the S&P 500’s largest historical declines—each followed by a sharp recovery in the 12 months that came next. The takeaway? Big drops are often the setup for big rebounds.

The Risk of Missing the Bounce

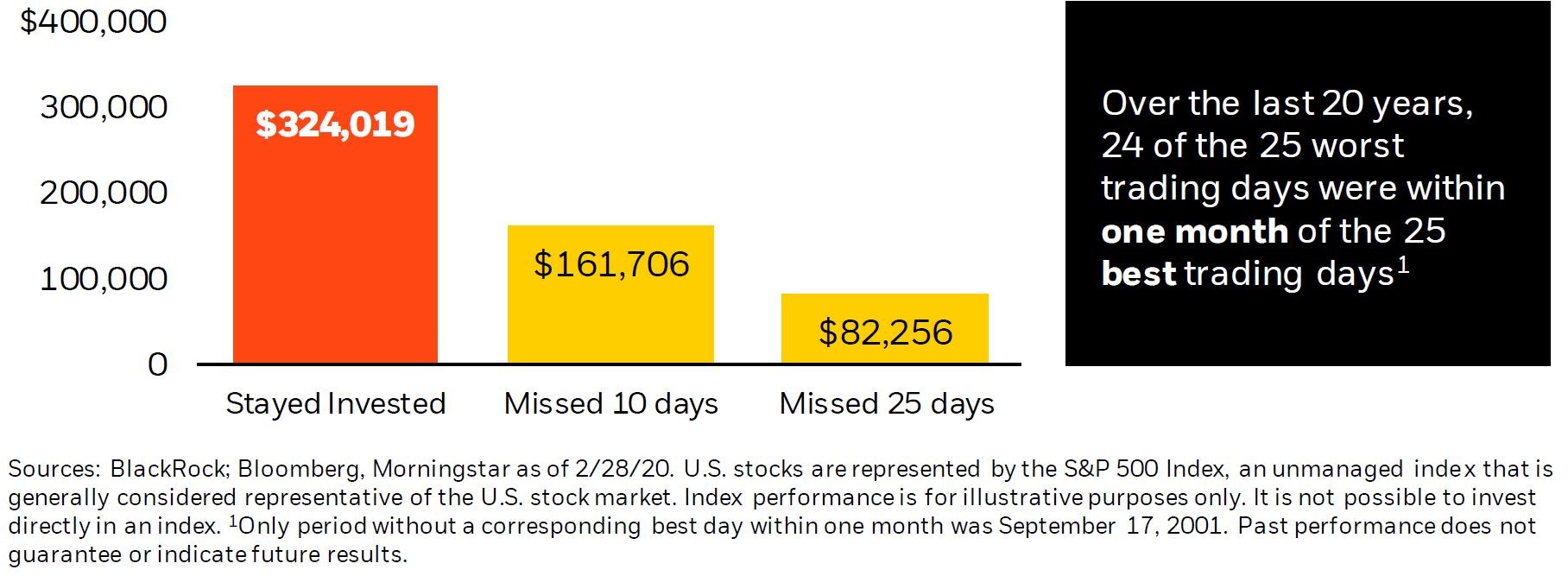

Consider this: The chart below shows that missing just a few days can make a huge difference. Between 2000 and 2019, a $100,000 investment in the S&P 500 would have grown to over $324,000. But if you missed just the 10 best days—often the ones that follow sharp drops—your return would be cut in half. Here’s the surprising part: the best and worst days tend to happen close together. In fact, 24 of the 25 worst days were within just a month of the 25 best days.

So what does that mean for your plan? Stepping to the sidelines “until things feel better” often leads to missing the very days that fuel long-term growth.

So… Should You Ever Make a Change?

Absolutely. But not because of headlines. We recommend filtering decisions through two clear, grounding questions:

-

Have your goals or needs changed? If life circumstances shift—retirement, sale of a business, a major health event—it’s worth revisiting your plan. Your goals are the foundation. The market should never override them.

-

Is your portfolio behaving as expected in this market? A properly built plan has purpose-built “buckets.” Your short-term needs should be protected from volatility. Your long-term assets are designed to weather storms and capture growth. If a 50/50 portfolio is acting like a 95/5 roller coaster, something’s off.

If your goals remain consistent and your portfolio is behaving as designed, that’s not a signal to change—it’s a sign that your plan is doing its job.

Final Thought: Clarity Over Reaction

Market turbulence can cloud judgment. But a thoughtful plan shines brightest in dark times. That’s why we build values-aligned, tax-smart, risk-aware strategies for our clients before volatility hits—so you can focus on your life, not the market’s mood.

Not sure if your plan is built to weather volatility?

Let’s talk through it together—clarity starts with a conversation.

Sources – Blackrock, Morningstar

Josh Whelan

CFP®, CLU®, ChFC®

Partner, Financial Advisor

About the Author

Josh sees his profession as a calling, not just a career. His motive for pursing financial planning was very personal. While working on a degree in marriage and family counseling, Josh’s father was diagnosed with multiple sclerosis. Josh decided then and there to change career paths to help his family prepare for an uncertain financial future. Financial planning became his path to serving others.

The “Alterra” name was coined by joining the Latin roots “alter”, the origin of the word “altruism” with “terra” meaning earth or land. This name reflects the company philosophy of “clients before profits” and providing firmly grounded advice.