How’s my portfolio doing? Is it beating the S&P 500? This is a common path that many investors take when evaluating their investment strategies, especially when a well-known index like the S&P 500 rallies ahead of many others. As one of the most widely recognized benchmarks, it’s common to compare your strategy against it – but should you? First, let’s take a closer look at the S&P 500 as a benchmark. Then, we’ll look at three principles to follow so you can confidently build and evaluate your strategies.

A look at the hidden risk of the S&P 500

The S&P 500 provides far more diversification than investing in a single stock, but about a quarter of your investment in the S&P 500 rests on the fate of Apple, Microsoft, Amazon, NVIDIA, and Google (now Alphabet). Why? These five companies make up about 21% of the S&P 500’s value. As a “capitalization-weighted” index, the S&P 500 tracks 500 US stocks, but the biggest companies carry the most weight. Overall, tech stocks make up more than 27% of the index. When tech rallies, the S&P will look great, but when tech suffers, the S&P will fall behind.

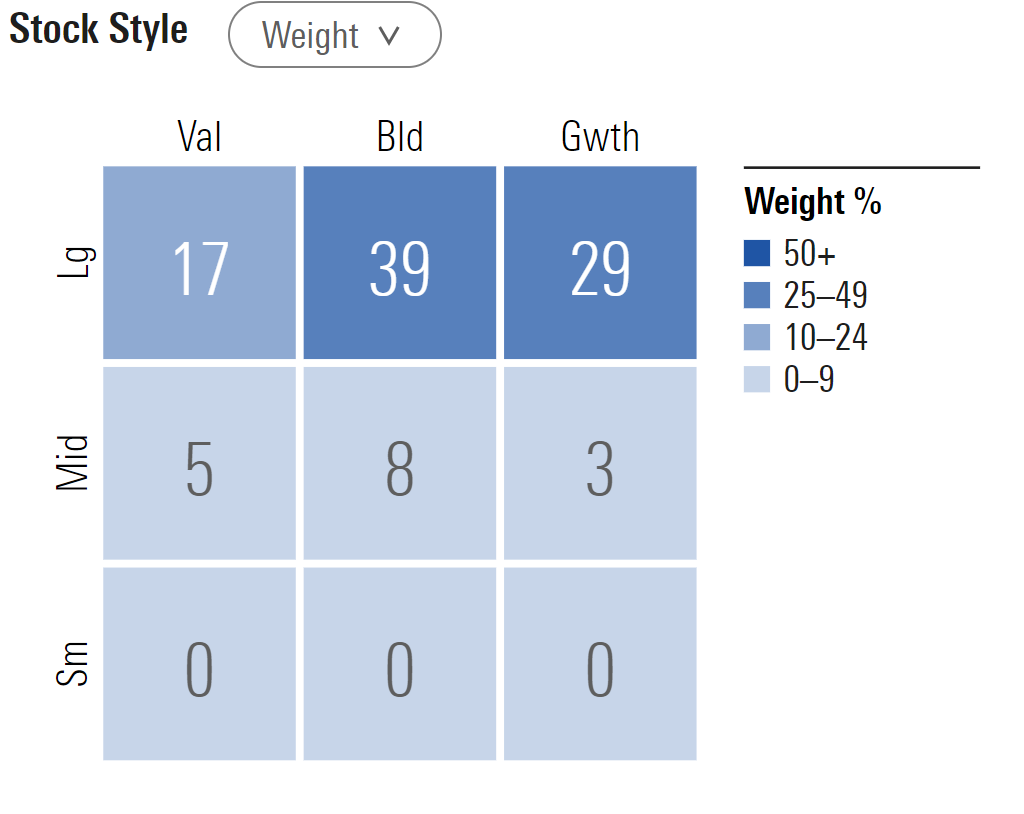

The S&P 500 is also dominated by large growth stocks, as shown here by Morningstar, meaning you have less invested in value stocks, which often pay higher dividends and lower volatility than growth stocks, and miss out entirely on small companies, which can fuel strong growth. We also regularly see big gaps in performance between growth stocks like Amazon and value or dividend stocks like Johnson & Johnson. Dividend stocks, though they tend to provide consistent income, reduced volatility, and can be a great addition to retirement portfolios, rarely make the list of top companies in the S&P 500.

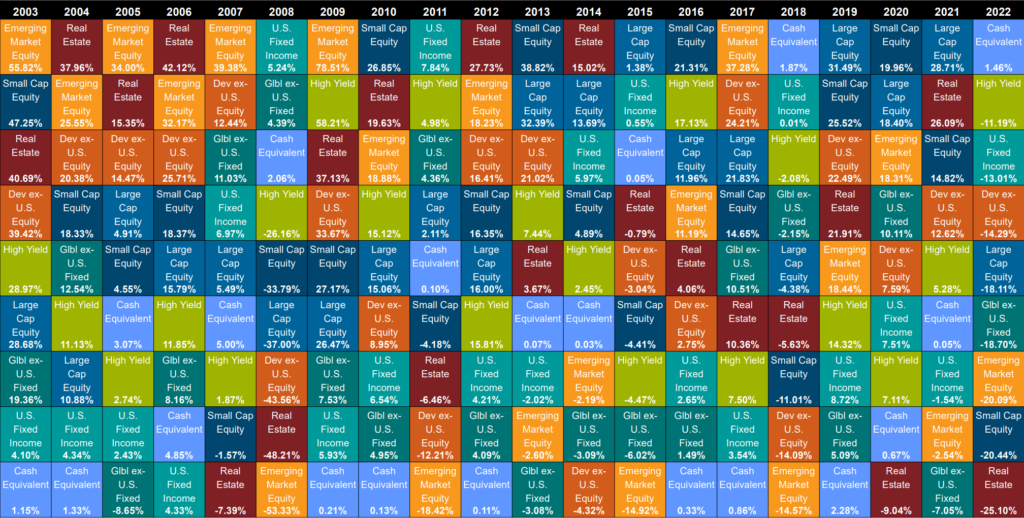

The Callan Periodic Table of Investment Returns – also called the “Investment Quilt chart” – shows us that these gaps don’t last forever. Compiled annually, the analysts at Callan Institute track returns of different categories of investments, often called asset classes. This chart assigns a color to each type of investment and ranks them top to bottom each year from highest to lowest return.

Build the right strategy…for you.

A portfolio manager at Russell Investments said “You can’t retire on a benchmark”. Your comprehensive strategy can’t ignore taxes and, more importantly, your goals. If the idea of having a quarter of your investment portfolio rest on the fate of five or six companies makes you uncomfortable, what should you do? Above all, start with your needs and build a diversified strategy accordingly. No one can consistently predict which stock or sector will win out next year, but we can focus on three key principles.

- Let your needs guide your strategy. Are you an aggressive investor focused on growth for 10 or more years? Your strategy might be invested entirely in stock, spread across US and international, growth and value, large and small companies. Or are you retired and need steady income today? Your strategy might be evenly split between stocks and bonds with a focus on dividend paying companies.

- Evaluate your portfolio against the right benchmarks. Your portfolio invested 20% in international stocks and 25% in bonds will look very different than an index invested 100% in US companies. A dividend focused strategy will not always track closely with a growth focused index. Look at your mix and use an appropriate blend of benchmarks.

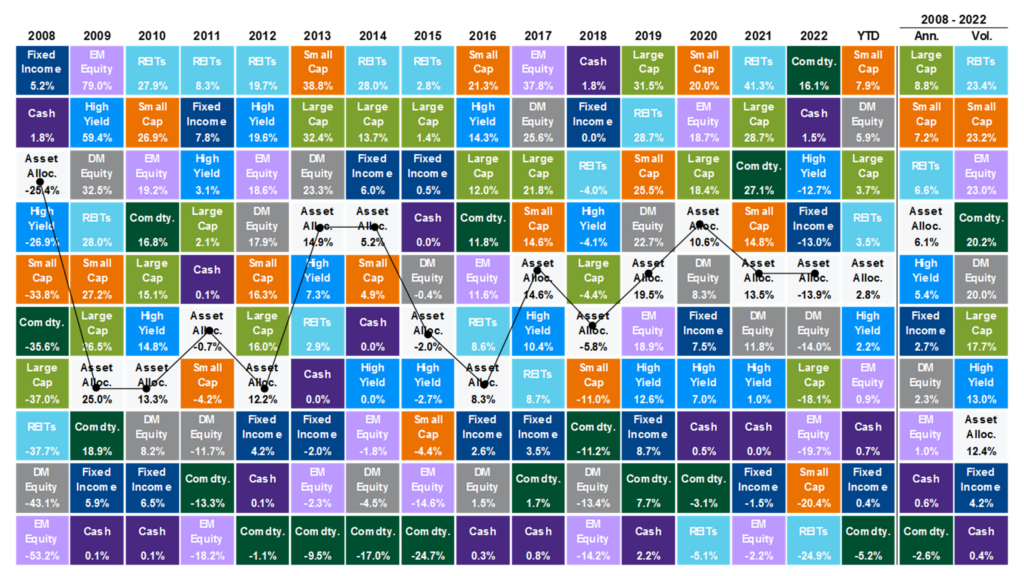

- Eliminate the guesswork. As the folks at the Callan Institute show, no asset class wins forever. Rather than shifting dramatically between assets each year, maintain a mix of asset classes throughout your investment life and make adjustments as your needs change. JP Morgan’s revised Investment Quilt chart below adds a diversified portfolio to make this point.

Benchmarks like the S&P 500 can be helpful guideposts, but don’t focus too much on any single index, as you’re likely to find yourself chasing past returns. Your portfolio strategy should be built around your needs. While no one has the crystal ball to tell exactly what the future holds, we do have a wealth of historical evidence of what works. These time tested habits put you in great position to reach financial independence and have peace of mind.

Ryan Colis

CFA, CFP®

Partner, Financial Advisor

About the Author

Ryan is a problem solver. He has a distinct ability to create a simple solution for very complex puzzles. So, naturally, he’s an integral part of our team. His favorite part of his role at Alterra is the analysis – whether analyzing a financial plan or reviewing an investment portfolio. However, the profession allows him to share that passion with clients by helping them navigate financial complexities as they collaborate on achieving their personal and financial goals.

After completing his undergraduate degree in Business Management, Ryan and Grant met by chance, developed a rapport and have been working together ever since. Ryan has continued his formal training in finance by earning his CFP and CFA designations.

The “Alterra” name was coined by joining the Latin roots “alter”, the origin of the word “altruism” with “terra” meaning earth or land. This name reflects the company philosophy of “clients before profits” and providing firmly grounded advice.